That’s My Quant: Indexing the DeFi Stablecoin-Network Frontier

Stablecoins are eating finance from the inside out. DeFi designs bring composability superpowers while fiat is suffocated by rent extraction and systemic drag. The OPEN Stablecoin Index tracks this frontier and lets time and governance do the compounding.

An index is a lighthouse in volatile seas. The Open Stablecoin Index ($OPEN) started with a simple thesis: track the next-gen networks building programmable money, then let time and governance do the compounding. Built on Ethereum using Reserve’s Index DTF rails, OPEN runs as an equal-weight basket of stablecoin governance tokens with quarterly rebalances (see current basket here). The method is deliberately simple, which is exactly the point.

Think of OPEN not just as an index but as a programmable primitive, composable in ways no traditional ETF can match.

On September 18, I sat down with fellow stablecoin enthusiasts — Nick from 512M Research, Joe from Pangea, and Gerrit from Curve Finance and Leviathan News. We compared notes on OPEN: what it buys, how it rebalances, where methodology should evolve, and how governance can harden. Below are highlights you may find a useful addendum to the recorded conversation.

Why an Index Now

Dollar-pegged stablecoins dominate onchain settlement. USDT sits above $170B and USDC near $74B, pulling liquidity into their orbit. Supply is still mostly dollar-denominated, yet the design space is in its 1st generation infancy.

Regulation is catching up. The GENIUS Act now defines rules for centralized payment stablecoins, while decentralized ones remain outside scope for now. Broader clarity is expected by summer 2026, covering categories, reserves, governance, and decentralization.

The U.S. Treasury projects stablecoins could expand to roughly $2 trillion by 2030, a tenfold jump from early 2025. Macro adds fuel: the Fed’s September rate cut rekindled risk appetite and onchain credit. Lower yields squeeze centralized issuers’ T-bill carry, in due time will push focus toward decentralized models that monetize secondary activity instead of bank interest.

Pragmatists want one-shot exposure to leading stablecoin ecosystems. Allocators tracking headlines still lack a clean, direct way in. DeFi stablecoins remain smaller, but they ride the same wave and drive frontier experimentation. Nearly every $OPEN constituent is shipping new features in the next 12 months. Early adopters capture alpha, while TradFi and regulators can integrate designs already stress-tested onchain.

Rising liquidity lifts every protocol that can float.

The OPEN Indexing Case

Indexing accepts that single names can drag the market, or worse. Programmatic weighting spreads exposure across multiple economic engines and tames the urge to “diamond-hand” a future zero.

Active selection chases sharper factor bets with higher risks, but a passive index cushions drawdowns and captures upside. Quarterly rebalances lock in gains from tokens that run ahead and top up those that lag, delivering a simpler process with far less psychological overhead than constant token picking.

Transparent onchain governance makes changes legible. Proposals, votes, and method tweaks are recorded onchain, reducing key-person risk and clarifying why constituents enter or leave. Over time the rules become the strategy, and the compounding comes from index discipline when sentiment swings.

What OPEN Actually Buys

OPEN tracks governance and ownership tokens of decentralized stablecoin networks. Its mandate emphasizes transparency, composability, and user-led governance. These include protocols where stable money is either the core product or the lubricant for the broader business.

Examples: Aave has GHO, but its main draw is the lending engine. Curve powers global stablecoin liquidity, while crvUSD adds stability optionality for collateral.

Even centralized stables began as accelerators, not businesses. Before rates became a profit engine, USDT drove Bitfinex volumes and USDC boosted Coinbase and Poloniex. At launch, these tokens were extensions of exchanges, not standalone ventures.

OPEN’s role is to track decentralized stablecoin demand wherever value accrues.

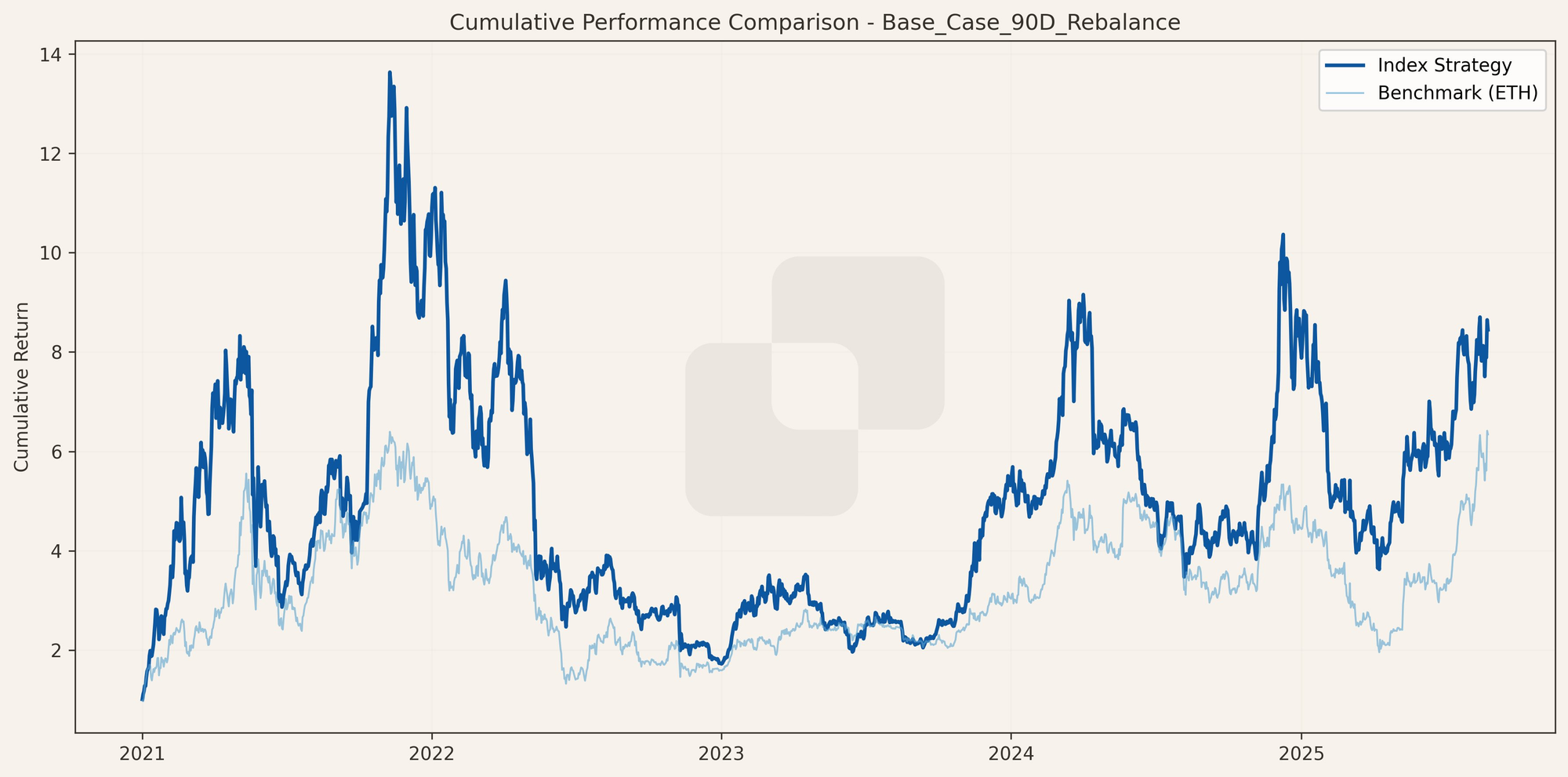

The Backtest, Read with Adult Supervision

512M’s reconstruction asked a simple counterfactual. What if OPEN had launched in 2021 and followed its current rules through today?

The headline result surprised even seasoned crypto veterans. In the four-year backtest, OPEN outperformed ETH by a wide margin, +745% total return versus +487% for ETH. That translates into almost double the annualized return, 37% compared to 17%.

By resetting each quarter, the index took profit from tokens that ran ahead and added to those that fell behind, while ensuring no single token could sink the basket.

512M’s take: excess return beyond simple ETH beta. Measured against ETH, OPEN shows stronger risk-adjusted returns across every ratio.

- Sharpe (0.49 vs 0.24) shows returns are earned more efficiently per unit of total volatility.

- Sortino (0.70 vs 0.33) highlights stronger protection from downside risk.

- Calmar (0.43 vs 0.18) underscores better rewards relative to maximum drawdowns.

- Treynor (0.45 vs 0.15) demonstrates three times the excess return per unit of market risk.

A “high-beta ETH trade” is an asset that simply exaggerates ETH’s moves, rising faster in rallies but crashing harder in pullbacks. OPEN is different: its performance profile shows it adds genuine diversification, making it a true portfolio building block rather than just levered ETH in disguise. For context, 5-year Sharpe ratios sit around 0.89 for the S&P 500, 0.70 for the Nasdaq Composite, and 0.73 for the Nasdaq-100.

Backtests are useful signals but come with limits. Running today’s basket retroactively bakes in survivorship bias: failed tokens like Terra Luna never appear, making returns look stronger than they would in real time. It also assumes governance would have made the same inclusion choices years ago, which is unlikely. A more faithful approach is to simulate historical inclusion rules with delistings, drawdowns, and token deaths factored in.

So treat backtest results as directional, not definitive. Most importantly, this post is not financial advice, and nothing here should be taken as a signal to buy OPEN.

Methodology, and How it Might Evolve

OPEN rebalances quarterly, balancing drift, execution costs, and governance overhead. Equal-weighting gives smaller constituents a chance, but alternatives are debated: inverse market-cap weighting, “gem index” tilts, or partial shifts into yield-bearing stables. These strategies aim to be rules-based smart beta. Market-cap weighting works in TradFi, but with only ten tokens would it hollow out OPEN, since investors could just hold the top three directly and skip index fees?

Scaling adds challenges. Rebalancing trades risk moving prices. That’s why CoW Swap auctions pool liquidity for MEV-protected trades within preset bounds. Liquidity screens must scale with market cap to avoid slippage. Bands also matter: current 1% and 40% limits keep small tokens alive but risk churn. 512M’s analysis suggests widening to 5%–45% and testing semiannual rebalances for efficiency.

Constituent emissions need scrutiny too. Inflation that outpaces adoption dilutes value. Governance should weigh unlock schedules, reward flows, and whether emissions land in real sinks like staking or buybacks. Programmatic, onchain emissions align with OPEN’s bullseye; opaque, offchain ones drift further.

OPEN’s methodology is a draft. Weighting, cadence, liquidity, and emissions all remain open to refinement through governance.

Why Decentralized Stables?

Centralized issuers dominate distribution, scale, and TradFi access. But permissioned minting slows usage, blacklist controls create freeze risk (problematic for the budding agentic economy) , and reserves rely on monthly attestations. Revenue comes from clipping bond coupons, a model regulators resist sharing with users.

Decentralized stablecoins flip the logic. They audit collateral every 12 seconds and monetize crypto volatility across cycles. When prices rise, users mint against growing collateral, generating fees. When prices fall, liquidations and trading lift keeper and AMM revenue. These programmatic flows create yield from market activity itself.

The kicker: DeFi income moves opposite to centralized issuers. Falling interest rates shrink TradFi margins but boost demand for leverage, CDP minting, and onchain fees.

These yields flow back to users and DAOs, enabling decentralized stablecoins and flatcoins to pressure centralized moats bound by rent seekers.

Let’s look at the potential for non-USD stablecoins, Euros and Swiss francs as an example. Demand is rising, but centralized issuers can’t make the math work. Near-zero or negative rates in Europe mean short-term bonds lose money, collapsing their model. Decentralized designs don’t face this constraint. They use onchain collateral and programmatic fees to support pegs in any rate environment. crvUSD and BOLD already prove fiat-pegged tokens can run entirely on decentralized collateral, free from bank deposits or government debt.

The agentic angle. Agentic AI won’t line up for KYC. It will spin up thousands of currencies, trade, shut down, and respawn. Central issuers choke on this workflow because mint and redeem run through compliance gates. Decentralized stablecoins fit machine-to-machine economies, letting agents mint, post collateral, and settle instantly without permission.

Composability is the Sleeping Giant?

Traditional ETFs sit under a single supervisory rule set across gatekeepers, limiting borrowing, option writing, and lending. Onchain indexes have more optionality, plugging into protocols as collateral, LP or vault receipts, and governance.

Onchain crypto has already proved this with the DeFi Pulse Index ($DPI), which hit ~$200M in 2021. Aave listed DPI as collateral, showing an index token can serve as usable money in DeFi, not just a passive tracker.

The breakthrough is consolidation: Instead of juggling ten volatile positions, each with different loan-to-value ratios and risk rules, one index position gives you diversified exposure under a single collateral umbrella. It simplifies borrowing, smooths risk, and frees up mental bandwidth. That’s the “a-ha!”: less overhead, same exposure, and better capital efficiency.

Composability then takes it further. You can hedge or shape exposure however you like. For example, hold the index for upside, short a perp to dampen drawdowns, or pair with yield stables to cover funding. Other builders can wrap these into structured products targeting income, lower volatility, or capped downside. Permissionless design accelerates the cycle.

Governance, Incentives, and the Bribe Question

Where there is voting power, bribes are not far behind. The Curve wars have already industrialized vote markets, so should OPEN expect copycats if market cap grows?

Bribes were flagged as both a potential feature and a risk. On one hand, they already exist across DeFi governance, and protocols eager for inclusion in OPEN may see it as rational to pay governors. If aligned with long-term incentives, such bribes might even help grow market cap without compromising outcomes. On the other hand, they carry obvious dangers: turning index governance into pay-to-play, encouraging the addition of low-quality tokens, and undermining the credibility of the methodology. The challenge is whether incentives can be structured so governors capture upside from a stronger index rather than short-term bribes.

OPEN-governance may also need governance hardening. When the SQUILL governance token market cap is less than the OPEN index market cap, a hostile buyer could try to rush a vote that stuffs the basket with low-quality tokens. This is a call to action on periodic risk analysis of quorum, time locks, and veto parameters.

What to Include Next

The point of OPEN is to track economic centers as they migrate, in a decentralized way. Tokenized CRCL equity is tempting but risks jurisdictional snarls and is far outside OPEN’s mandate of transparency, composability, and user-led governance.

A live question: should OPEN also include infrastructure protocols that materially expand stablecoin liquidity, utility, or safety? Convex is a candidate. The test: is the impact measurable onchain and tied to stablecoin flows?

An ongoing monumental task for the community is sharpening methodology rules. Clear rules of the road, consistently applied, often become the highways that enable wider scale and collaboration.

OPEN is both ticker and narrative. It tells the story of decentralized stable-money infrastructure eating legacy finance from the inside out. OPEN runs without a CEO or company, powered purely by smart contracts and community. Come for diversification, stay for composability.

This post is an open invitation: if you have sharper ideas, join us in refining this onchain index experiment. Follow on 𝕏, see what’s new in OPEN governance and drop into the OPEN Secret Admirers chat.

Or mint $OPEN to climb the learning curve faster!